Transparency Is Not Centralisation: NAR, DAR, and the Legal Architecture of Blockchain Governance

On court-order compliance, the CLARITY Act's maturity test, and why published rules are the opposite of discretionary control

I. Introduction

A former employee of the BSV Association has published allegations that the Network Access Rules (NAR) and Digital Asset Recovery (DAR) framework create a centralised governance structure exposing BSV to classification as a security under United States law. The argument runs as follows: a single entity — the BSV Association — exercises discretionary, off-chain authority over the network through binding Alert Messages and enforceable Network Access Rules. Miners must obey or face exclusion. One individual funds the dominant miner, core development, application infrastructure, media channels, and the Association itself. Therefore, when NAR and DAR are layered on top of this concentration, BSV presents “the exact profile regulators evaluate under the Howey framework.”

These claims are wrong on every material point of law, though the policy concern that underlies them — that concentrated ecosystem funding creates dependency risk — is legitimate and worth addressing on its own terms. The claims are wrong because they mischaracterise what NAR and DAR actually do. They are wrong because they misapply the legal tests they invoke. And they are wrong because they ignore the far more concentrated — and far less transparent — governance structures operating on the very networks that regulators have provisionally treated as decentralised.

This essay does five things. First, it explains the actual legal mechanics of DAR and NAR as set out in the published documents — not as characterised by someone with a grievance. Second, it analyses the real-world operation of court orders: how long they take, what they cost, and why the suggestion that DAR enables casual or rapid intervention misunderstands the procedural realities of cross-border litigation. Third, it examines the CLARITY Act’s “mature blockchain system” definition and its application to BSV, BTC, and Ethereum. Fourth, it considers the Howey framework and its application to stewardship models. Fifth, it explains why on-chain secret-ballot governance — the alternative that critics implicitly prefer — is not merely inadequate but actively dangerous, creating precisely the kind of concentrated, opaque control that securities regulators are designed to prevent.

The thesis is narrow and defensible: DAR is better characterised as transparent, legally mediated enforcement of property rights than as discretionary centralised control. That characterisation does not resolve every question about BSV’s regulatory status — questions which remain open and fact-sensitive — but it does demonstrate that the former employee’s claims rest on a fundamental mischaracterisation of the primary documents.

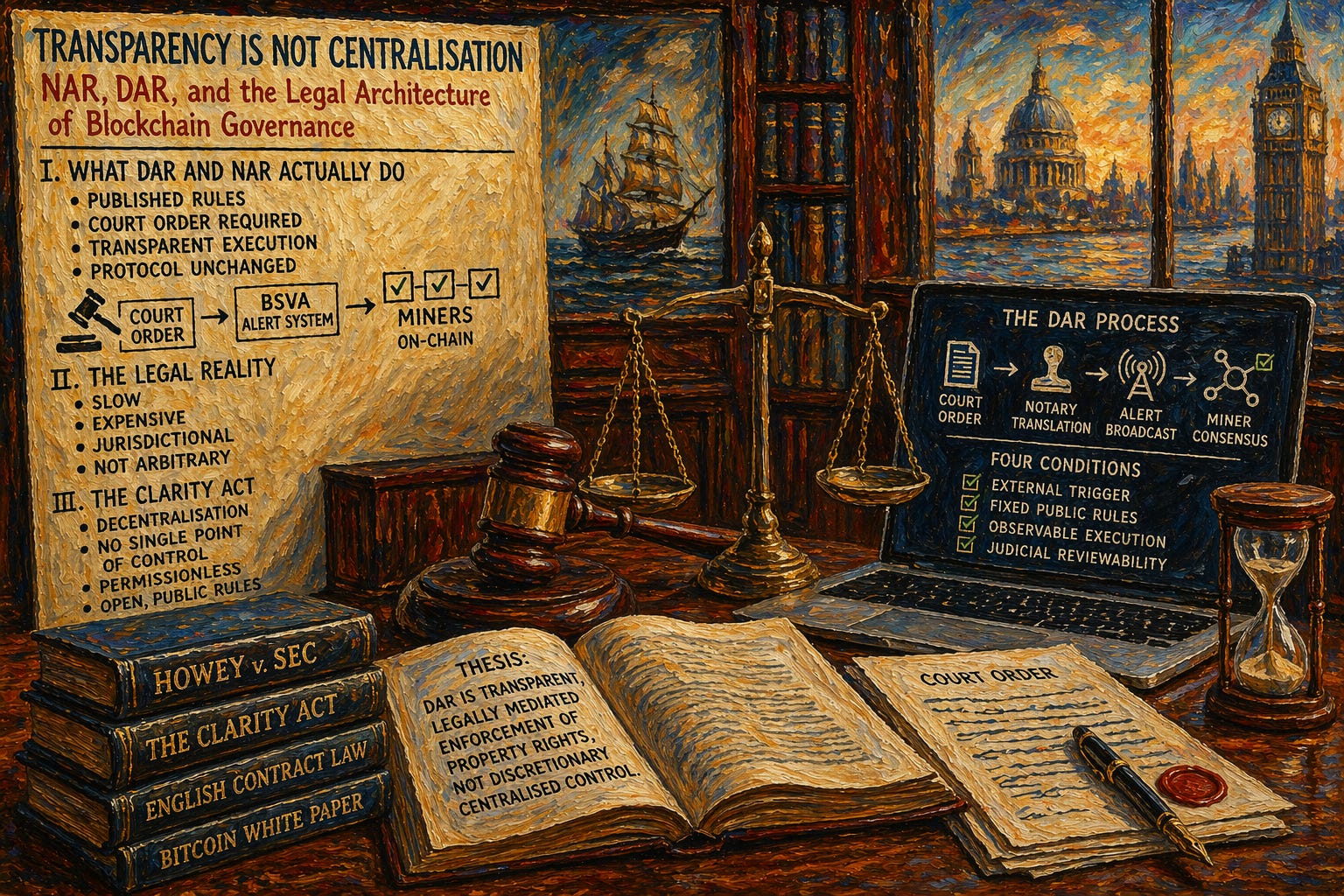

II. What DAR and NAR Actually Do

The Network Access Rules

The NAR is a published set of rules regulating the relationship between the BSV Association and nodes on the BSV network (BSV Association, ‘Network Access Rules’, Version 1, 15 February 2024, available at nar.bsvblockchain.org). The rules are grounded in the principles of the Bitcoin white paper (S. Nakamoto, ‘Bitcoin: A Peer-to-Peer Electronic Cash System’, 2008) and operate through the legal doctrine of the unilateral contract.

A unilateral contract in English law arises where an offer is made to an indefinite class and acceptance occurs by performance of the specified act, without any need for prior communication of acceptance, provided the offer is sufficiently certain and evinces an intention to be legally bound: Carlill v Carbolic Smoke Ball Co [1893] 1 QB 256 (CA). The paradigm is the reward case: the offeror stipulates conditions, the offeree performs, and performance crystallises the bargain (Williams v Carwardine (1833) 5 C & P 566).

The BSV Association’s own documentation draws on the case of Clarke v Earl of Dunraven (The Satanita) [1897] AC 59, in which the House of Lords held that competitors in a yacht race were contractually bound to one another by the racing association’s rules, despite never having communicated directly. Each competitor “sailed into” the contract by entering the race. The analogy to mining is illustrative, though not perfectly congruent — a globally distributed technical network with heterogeneous participants, multiple software implementations, and contested jurisdictional reach is not identical to a yacht race. The case establishes the principle that participation in a rules-governed activity constitutes acceptance of those rules, not that the factual matrix of nineteenth-century yacht racing maps precisely onto twenty-first-century distributed computing. The operative point is that the NAR is published before participation begins. It is available to any prospective miner. No miner is compelled to join. No miner is prevented from reading the terms before committing hashpower.

The NAR is also a bilateral instrument. It does not merely stipulate what the Association expects of nodes. It stipulates what nodes may expect of the Association. It constrains the steward as much as the participants. The Association cannot alter the protocol — the protocol is locked, fixed, “set in stone.” The NAR codifies obligations that were always implicit in the white paper’s definition of honest nodes. It makes explicit what was previously unwritten. That is transparency, not centralisation.

Digital Asset Recovery

DAR enables the freezing or reassignment of digital assets on the BSV blockchain. The critical structural feature — systematically understated in the former employee’s public statements — is that DAR requires a court order valid and enforceable under English or Swiss law.

The BSV Association has stated explicitly: “The BSVA does not intend to act as a judge in any way, and directives are only issued when there is an applicable court order recognised as valid and enforceable by Swiss or English law authorities” (BSV Association, ‘Protecting Assets, Ensuring Justice: BSVA’s Alert System and DAR Framework’, 2024).

The process operates in four defined steps:

A plaintiff initiates legal proceedings to establish ownership of the assets in question.

The plaintiff obtains a freeze order, injunction, or equivalent instrument from a court of competent jurisdiction.

A designated notary translates the court order into a machine-readable format and broadcasts it to the mining network via the Blacklist Manager.

Miners receive the broadcast, confirm receipt, and — upon sufficient consensus among honest nodes — the freeze is activated at the network level.

Foreign court orders must first be recognised in England or Switzerland through established private international law mechanisms before they can be transmitted through the system.

A question arises about the nature of miner compliance. Is participation in DAR voluntary or compelled? The honest answer is that it is contractually obligated under the NAR, but not physically coerced. A miner who refuses to comply with a validly transmitted court order is in breach of the NAR — the rules they accepted by commencing mining. The consequence is that their blocks may be orphaned by the rest of the network if they include transactions spending frozen UTXOs, because compliant nodes will reject those blocks. This is not dissimilar to the position of a bank employee who refuses to implement a Mareva injunction: the refusal does not prevent the injunction from taking effect; it exposes the non-compliant party to legal and operational consequences.

The system is therefore neither purely voluntary nor coercive in the criminal-law sense. It is contractually structured compliance within a rule-bound framework. Miners are free not to mine BSV. They are free to read the NAR before committing hashpower. But if they choose to mine BSV, they accept the published rules — including the obligation to comply with judicially authorised directives transmitted through the alert system. This is the same structure by which any participant in a regulated market accepts the rules of that market as a condition of participation.

The former employee frames this as “miners must obey or they’re out,” implying arbitrary exclusion. The more accurate characterisation is that miners must comply with court orders or their blocks will be rejected by the consensus of honest nodes — which is precisely how the white paper’s definition of honest nodes was always intended to operate.

This is not discretionary authority. It is court-order compliance mediated through a transparent technical process. The Association does not decide who owns what. Courts decide. The Association transmits the court’s decision to the network. This is functionally identical to what every bank, every brokerage, every financial institution in the world does when it receives a court order — except that the process is published, the rules are public, and the mechanism is visible to every participant on the network.

The former employee describes this as “off-chain, discretionary control by one entity.” Every element of that characterisation requires scrutiny. It is not discretionary — it requires a court order. The “one entity” does not make the decision — the court does. And describing court-order compliance as “off-chain control” is like describing a bank’s compliance with a Mareva injunction as “off-ledger control.” It is technically accurate in the most trivial sense and substantively misleading in every sense that matters.

The Alert System

The Alert System is a reimplementation of the alert key mechanism that was part of Bitcoin’s original design. Satoshi Nakamoto included an alert key in the earliest versions of the Bitcoin software, enabling a trusted party to broadcast warnings about critical vulnerabilities or network attacks (Bitcoin source code, version 0.1.0, 2009; discussed in Wright, Fiduciary Governance of BTC Core under English Law (University of Leicester, PhD thesis, 2025), §3.3.1). BTC Core developers removed this feature. The BSV Association restored it.

Alert messages can be notifications — software update announcements, for example — or directives, such as freeze, unfreeze, or reassign commands for transaction outputs. Directives are issued only pursuant to court orders. The system operates in conjunction with the NAR: it is the enforcement mechanism for judicially authorised actions, not a tool for discretionary intervention by the Association.

III. The Legal Reality of Court Orders

The suggestion that DAR enables rapid, unilateral asset seizure reveals a fundamental misunderstanding of how courts operate. A court order directing the freeze or reassignment of digital assets is not obtained by filing a form. It is obtained through adversarial litigation subject to the full procedural protections of the relevant jurisdiction.

England and Wales

Interim freezing injunctions are governed by CPR Part 25 and the principles established in Mareva Compania Naviera SA v International Bulkcarriers SA [1975] 2 Lloyd’s Rep 509 (CA). The applicant must demonstrate: (i) a good arguable case on the merits; (ii) a real risk of asset dissipation; and (iii) that the balance of convenience favours granting the order (American Cyanamid Co v Ethicon Ltd [1975] AC 396 (HL)). Even ex parte (without-notice) freezing orders must be followed by a return date — typically within seven to fourteen days — at which the respondent can challenge the order. The applicant must give a cross-undertaking in damages, accepting personal liability for losses if the injunction is later found to have been wrongly granted (Cheltenham & Gloucester Building Society v Ricketts [1993] 1 WLR 1545).

For a final order directing reassignment of assets, the claimant must succeed at trial. English High Court trials in commercial disputes involving digital assets routinely take twelve to thirty-six months from issue of proceedings to trial, and that assumes no jurisdictional challenges. Appeals under the Senior Courts Act 1981, s. 16, can add a further twelve to eighteen months.

The United States

Preliminary injunctions are governed by Federal Rule of Civil Procedure 65 and the four-factor test in Winter v Natural Resources Defense Council 555 U.S. 7 (2008): (i) likelihood of success on the merits; (ii) likelihood of irreparable harm absent injunctive relief; (iii) that the balance of equities tips in the movant’s favour; and (iv) that the injunction is in the public interest. Temporary restraining orders (TROs) can be obtained ex parte under FRCP 65(b), but they expire within fourteen days and must be followed by a hearing on the preliminary injunction. The full litigation timeline for a contested federal action involving digital asset ownership is comparable to England: eighteen months to three years for trial, longer with appeals.

Cross-Border Complexity

For DAR to operate on foreign court orders, recognition proceedings must be completed under the Hague Convention on Choice of Court Agreements 2005, bilateral treaties, or the common law rules articulated in Adams v Cape Industries plc [1990] Ch 433 (CA). The respondent can challenge recognition on grounds including lack of jurisdiction in the originating court, public policy objections under the relevant convention or statutory regime, and failure of proper service. These proceedings routinely consume twelve to twenty-four months. This introduces an entire additional layer of contested litigation before DAR can even be triggered.

Costs and Practical Constraints

The costs involved create a powerful economic constraint on DAR’s use. English High Court litigation costs for a contested freezing injunction application alone typically run to £50,000–£150,000 in solicitors’ and counsel’s fees. A fully contested cross-border asset recovery claim involving multiple jurisdictions, expert evidence on foreign law, and forensic tracing of digital assets can reach £1–5 million. In the United States, comparable federal litigation costs are broadly similar, often higher.

The economic implication is that DAR is overwhelmingly likely to be invoked only for claims involving assets of significant value — realistically, millions of pounds or dollars. This is not to say that subsidised claimants, strategic plaintiffs, litigants pursuing matters of principle, regulators with enforcement budgets, or rights-holders with legal expenses insurance could never invoke the process for smaller amounts. They could. But the economic structure of cross-border litigation creates a gravitational pull toward high-value claims that is difficult to overcome. The cost of the process is itself a constraint on its use.

Public Scrutiny: The Open Process

Every step of this process is public. Court filings in England and Wales are public documents (CPR r. 5.4C). Judgments are published. The court order transmitted to the network is visible to every miner. The broader community can scrutinise the order, its legal basis, and the authority under which it was issued.

This constitutes, in practical effect, a form of open, adversarial, judicially supervised scrutiny of property-rights disputes — conducted by courts applying centuries of developed jurisprudence, with full rights of defence and appellate oversight. It is not peer review in the academic sense — courts are adjudicatory institutions, not reviewers — but it is public, adversarial, and subject to layers of scrutiny that no on-chain governance mechanism replicates.

Compare this to what happens on BTC when assets are stolen. Nothing. The victim has no recourse through the protocol. They can file a police report. They can hire a blockchain analytics firm. They can attempt to identify the thief and sue them personally — assuming they can identify them, establish jurisdiction, and afford the litigation. But the protocol itself offers no mechanism for recovery, no matter how clear the evidence of theft, no matter how unambiguous the court order. This is not a feature. It is a failure of design — a failure that DAR was built to remedy.

IV. The CLARITY Act and the “Mature Blockchain System” Test

What the Act Says

The CLARITY Act (H.R. 3633, 119th Congress, 2025–2026), as reported by the House Committees on Financial Services and Agriculture in June 2025, defines a “mature blockchain system” as “a blockchain system, together with its related digital commodity, that is not controlled by any person or group of persons under common control” (§101(31)). Arnold & Porter’s analysis identifies four maturity requirements: (1) functional for executing transactions, accessing services, or participating in validation or decentralised governance; (2) composed of open-source code; (3) operating upon pre-established, transparent rules; and (4) not subject to the control of a single person or group, including by holding 20% or more of the tokens (Arnold & Porter, ‘Clarifying the CLARITY Act’, August 2025).

The former employee quotes this definition and argues that the combination of NAR/DAR and concentrated ecosystem funding means BSV fails the test. This analysis is deficient for three independent reasons.

Court-Order Compliance Is Not “Control”

The CLARITY Act uses “control” in the context of unilateral authority to alter rules or functionality — the same sense in which the term is used in securities regulation generally (see, e.g., Securities Exchange Act of 1934, §13(d), governing beneficial ownership and control). The BSV Association cannot alter the protocol. It cannot change the block size, the supply schedule, the scripting language, or the consensus mechanism. It can transmit judicially authorised directives through a published system.

Complying with court orders is not “control” in the securities-law sense. It is legal compliance. Every financial system in existence complies with court orders. Banks comply with freezing injunctions. Brokerages comply with SEC enforcement orders. Exchanges comply with OFAC sanctions lists. If compliance with judicial process constituted “control” sufficient to trigger the CLARITY Act’s maturity exclusion, then every regulated financial instrument in existence would fail the test.

It is important to acknowledge, however, that a regulator or hostile counterparty could argue that functional control extends beyond protocol specification to encompass the power to alter the spendability of specific UTXOs through the alert-blacklist pipeline. That argument has force. The response requires a careful distinction — set out in Section VII below — between alteration of consensus rules, alteration of transaction-validity conditions, and enforcement actions within an unchanged protocol framework. The regulatory treatment of that distinction under the CLARITY Act remains untested.

The Full Maturity Test

BSV is relatively well positioned against the full set of maturity criteria. The protocol is functional and processes transactions at enterprise scale. The code is open source. The rules — including the NAR — are pre-established, published, and transparent. The protocol is locked and cannot be altered by any party, including the Association. Whether BSV would be formally certified as mature under the Act is a question that depends on fact-sensitive regulatory analysis that has not yet occurred. But the structural features of BSV’s governance are more compatible with the maturity criteria than those of its principal competitors, for the reasons that follow.

The 20% Ownership Threshold

The CLARITY Act’s 20% threshold refers to token ownership, not infrastructure funding. The former employee conflates funding ecosystem infrastructure — mining operations, development, applications — with controlling the token supply. These are different legal categories. An investor who funds mining operations does not thereby “control” the protocol any more than a venture capitalist who funds a software company “controls” TCP/IP. The distinction between capital deployment and protocol control is fundamental to securities analysis and should not be elided.

V. BTC Core: The Centralisation That Nobody Discusses

The irony of the former employee’s position deserves examination. He argues that BSV is too centralised because the BSV Association transmits court orders through a published framework. Meanwhile, BTC Core — which he does not critique — operates under a governance structure that is centralised by any reasonable definition and transparent by none.

BTC Core is governed by a small group of developers with commit access to the GitHub repository who exercise effective authority over the Bitcoin Core reference client (Wright, Fiduciary Governance of BTC Core under English Law (University of Leicester, PhD thesis, 2025; forthcoming as peer-reviewed monograph, Ethics Press, 2026), chs. 4–5). As of January 2026, following the addition of the developer known as “sedited” (TheCharlatan), the group of maintainers with commit access numbered approximately five or six individuals (bitcoin++, ‘Bitcoin Core Adds New Maintainer: sedited’, 10 January 2026). Bitcoin Core’s own contributing guidelines acknowledge that “there are repository maintainers who are responsible for merging pull requests, the release cycle, and moderation” (bitcoin/bitcoin, CONTRIBUTING.md, GitHub). These maintainers are “the only ones who have the ability to make changes to the codebase that is shipped as bitcoin-core to users” (ibid.).

This concentration of commit authority is not merely a thesis advanced by the present author. Angela Walch, in her widely cited chapter ‘In Code(rs) We Trust: Software Developers as Fiduciaries in Public Blockchains’ (in Hacker, Lianos, Dimitropoulos and Eich (eds), Regulating Blockchain: Techno-Social and Legal Challenges (OUP, 2019)), argues that leading developers of public blockchains “function much like fiduciaries of those who rely on these powerful data structures,” and that “this power was largely unacknowledged, undefined, and unaccountable.” Walch’s analysis — developed independently of the present author’s work — reaches a structurally similar conclusion: that the decentralisation narrative masks concentrated developer authority that creates fiduciary-like obligations. Her work has been cited over 1,000 times and presented at Harvard Law School, Stanford, and the Bank of England.

There is no published governance framework equivalent to the NAR. There is no contractual instrument binding developers to users or miners. There is no court-order compliance mechanism. Developers receive financial support from commercial sponsors — Blockstream, Chaincode Labs, the Human Rights Foundation, Square, and others — under arrangements that are not governed by any published conflict-of-interest policy (Wright, §§4.3.1–4.3.3).

These developers have implemented protocol-level changes including SegWit (BIP 141, activated August 2017), which altered the transaction format; Replace-by-Fee (BIP 125), which changed mempool policy; and the maintenance of the 1MB block size cap over the objections of a significant portion of the mining and user community (Wright, §§5.2–5.3). The Taproot upgrade (BIP 340–342, activated November 2021) was activated through the Speedy Trial mechanism, in which signalling was effectively determined by five major mining pools (Wright, §5.4.1). These are not implementation tweaks. They are protocol-level changes imposed by a developer group operating without published governance rules, without contractual constraints, and without any mechanism for users or miners to enforce accountability.

As I have demonstrated in my thesis, BTC Core satisfies the statutory definition of a partnership under the Partnership Act 1890, s. 1(1) — “persons carrying on a business in common with a view of profit” — with the consequence that developers owe fiduciary duties of loyalty, care, and good faith to network participants. Breaches — such as implementing self-serving protocol changes or failing to address critical vulnerabilities — could trigger remedies including the imposition of constructive trusts or the disgorgement of profits gained through breach (Wright, chs. 6–7).

The analytical point is this: BSV’s governance is visible because it is published, constrained, and legally defined. BTC’s governance is invisible because it is informal, unpublished, and operates through personal relationships and undisclosed financial interests. If the CLARITY Act’s “control” test is applied consistently, a system where a handful of developers can change the protocol at will, funded by commercial sponsors with undisclosed financial interests, raises serious questions about control by “a group of persons under common control.”

VI. Ethereum: Decentralisation by Decree

Ethereum presents the same structural problem in a different form. The Ethereum Foundation — a Swiss non-profit — functions as the de facto steward of the Ethereum protocol. Vitalik Buterin occupies a role in Ethereum governance that has no equivalent in any other major blockchain. He selects the Foundation’s leadership. He defines the Foundation’s mandate. He determines the protocol’s development priorities.

Buterin stated in January 2025: “The person deciding the new EF leadership team is me. One of the goals of the ongoing reform is to give the EF a ‘proper board’, but until that happens, it’s me” (X post, 21 January 2025). In December 2025, Buterin published a governance analysis acknowledging that “centralized entities now exert excessive influence over protocol upgrades, client diversity and Layer 2 operations,” with over 60% of staked ETH controlled by a few teams (Bitget News, 30 December 2025, reporting on Buterin’s governance post). In March 2026, the Foundation published a new mandate — authored by Buterin — defining Ethereum as “sanctuary technology” and the Foundation’s role as its steward.

The Ethereum Foundation holds a substantial treasury of ETH tokens. It funds development teams, grants programmes, and ecosystem initiatives. Its decisions about what to fund and what not to fund shape the protocol’s evolution. And there is no published contractual framework — nothing equivalent to the NAR — governing the relationship between the Foundation, validators, and users. There is no court-order compliance mechanism. There is no published process for asset recovery.

The Ethereum Foundation has changed the protocol fundamentally and repeatedly. The DAO hard fork in 2016 reversed completed transactions to recover funds from a hack — a far more interventionist action than anything DAR contemplates. At the time of the attack, the DAO held 14% of all Ethereum ever issued (Wright, §2.2.3; Zou, ‘Cryptocurrency and Blockchain Governance’ in Regulation of Crypto-Assets (Hart Publishing, 2024)). The decision to fork was made through an informal process driven by the Foundation and by Buterin personally — without a court order, without adversarial process, without any published framework constraining the decision, and without any formal mechanism for affected parties to challenge it. The Merge in 2022 replaced the entire consensus mechanism from proof-of-work to proof-of-stake. These are not maintenance updates. They are architectural transformations imposed by a foundation under the effective control of one individual.

The DAO fork is particularly instructive because it represents exactly the kind of discretionary, centralised intervention that the former employee purports to identify in BSV — except that it was executed without judicial process, without published rules, and without any constraint on the Foundation’s authority. DAR, by contrast, operates only through court orders, with full adversarial process, cross-undertakings in damages, and appellate oversight.

If BSV’s published, court-order-constrained, protocol-locked governance structure raises concerns under the CLARITY Act’s maturity test, then Ethereum — where one person decides the foundation’s leadership, the foundation changes the consensus mechanism, and no published contractual framework constrains any of it — raises far graver ones.

VII. The Howey Test

The former employee invokes the Howey four-factor test — SEC v W.J. Howey Co. 328 U.S. 293 (1946) — arguing that NAR/DAR creates “the exact profile regulators evaluate.” The test requires: (1) an investment of money; (2) in a common enterprise; (3) with an expectation of profits; (4) derived from the efforts of others.

The relevant prong is the fourth: profits derived from the efforts of others. The argument is that BSV holders rely on the BSV Association’s stewardship — its alerts, its rule enforcement, its governance decisions — and that this reliance constitutes dependence on the “efforts of others.”

SEC v Ripple Labs Inc (SDNY, 2023) clarified that programmatic secondary-market sales of tokens do not satisfy the “efforts of others” prong where purchasers do not reasonably expect to profit from the issuer’s continuing entrepreneurial or managerial efforts. The BSV Association’s role under NAR/DAR is not entrepreneurial or managerial. It does not develop the protocol (the protocol is locked). It does not build applications. It does not market BSV to investors. It maintains the integrity of a fixed technical specification and transmits court orders. This is functionally closer to a standards body maintaining a technical standard — ISO, IEEE, IETF — than to a promoter whose ongoing efforts generate value for investors.

However, the Howey analysis is inherently fact-sensitive and contextual. Whether a particular purchaser’s expectations were shaped by reliance on organised stewardship, legal recoverability, infrastructure support, and ecosystem financing is an empirical question that cannot be resolved in the abstract. A critic would argue that the essay underplays ecosystem reality: if purchasers are induced to expect value from ongoing stewardship, the “efforts of others” question becomes more complicated than a simple categorical exclusion can capture.

This objection deserves engagement rather than dismissal. The question is what shapes purchaser expectations in practice. Under Howey and its progeny, the relevant inquiry is whether the promoter’s efforts are “the undeniably significant ones, those essential managerial efforts which affect the failure or success of the enterprise” (SEC v Glenn W. Turner Enterprises Inc. 474 F.2d 476 (9th Cir., 1973)). The BSV Association’s stewardship — maintaining a locked protocol, transmitting court orders, publishing governance rules — is administrative and custodial, not entrepreneurial. It does not determine the commercial success or failure of BSV as a network. Commercial success depends on adoption, application development, transaction volume, and market dynamics — none of which the Association controls or directs.

To be clear: the existence of DAR (legal recoverability) and NAR (published governance) may well contribute to purchaser confidence. But confidence derived from the existence of a legal framework is not the same as reliance on managerial efforts. Investors in publicly traded equities derive confidence from the existence of the SEC’s enforcement apparatus, but that does not make the SEC a “promoter” whose efforts satisfy the fourth Howey prong. The distinction between institutional infrastructure that supports a market and entrepreneurial activity that drives returns is well established in securities jurisprudence. DAR and NAR fall on the infrastructure side of that line.

The stronger claim is not that the Howey analysis conclusively favours BSV. It is that the former employee’s confident assertion that BSV presents “the exact profile” is not supported by the legal authorities he invokes, and that the same analysis — if applied with equal rigour — would raise more serious questions about BTC and Ethereum, where developer and foundation efforts in changing the protocol are demonstrably more entrepreneurial in character.

VIII. Why On-Chain Governance Is Not the Answer

The implicit alternative to NAR/DAR — the model preferred by the crypto-anarchist tradition — is on-chain governance through token-holder or hashpower-weighted voting. This model introduces governance risks that are at least as serious as those the former employee attributes to BSV’s current structure — and in important respects, more serious, because they are less transparent.

The Hashpower Problem

On-chain governance mechanisms that use proof-of-work signalling — BIP 9 activation, for instance — are susceptible to gaming by concentrated hashpower. A miner controlling 30% of the network’s hashpower can veto any proposal that requires supermajority signalling. A miner controlling 51% can impose any proposal unilaterally. This is not theoretical. The SegWit activation on BTC involved precisely this dynamic: BTC Core developers circumvented miner signalling through the User Activated Soft Fork (UASF) mechanism when miners declined to signal support (Wright, §5.4.1) — demonstrating that the “decentralised governance” narrative was a fiction even on BTC’s own terms.

Secret Ballots and Governance Coalitions

On-chain voting mechanisms that use token-weighted or stake-weighted ballots create a more dangerous concentration risk. A party controlling a large amount of hashpower or stake can engage in what amounts to a secret ballot — their vote is visible on-chain, but the agreements, side payments, and coordination behind it are not.

Consider a concrete scenario. Two mining pools collectively control 55% of hashpower. They enter into a private agreement to coordinate their governance votes on all protocol proposals. This agreement is entirely off-chain — it could be a handshake, an encrypted message, a verbal understanding. On-chain, their votes appear independent. In reality, they constitute a controlling coalition that can determine every governance outcome.

This is not transparency. It is the illusion of decentralisation masking actual concentrated control — precisely what securities regulators are designed to detect. And because the coordination is private, there is no public scrutiny, no adversarial process, no judicial review, and no accountability mechanism. The coalition can act in its own interest, against the interests of other participants, with no recourse available to the minority.

The 50% Problem

The problem compounds at the 50% threshold. If governance decisions are made by majority hashpower vote, then any coalition controlling 50%+1 of hashpower controls all governance outcomes. This coalition can be assembled through private agreements on large hash transfers — agreements that are invisible to the rest of the network. The result is a system that appears decentralised but is, in fact, governed by an invisible oligarchy whose membership, agreements, and financial interests are unknown to the network.

This is precisely the structure that the CLARITY Act’s maturity test is designed to identify: control by “a group of persons under common control.” And it is harder to detect in an on-chain voting system, where coordination is private, than in a published governance framework like NAR, where the rules, the authority, and the constraints are visible to all participants.

Stake-Weighted Voting

Proof-of-stake governance compounds the problem further. Stake-weighted voting concentrates governance authority in proportion to wealth. As Cappiello and Carullo have noted in the context of Cardano, technical literacy requirements may exclude less-informed stakeholders, while stake-based voting concentrates influence in financially dominant participants (discussed in Wright, §2.2.3). This creates what Bauwens, Kostakis, and Pazaitis describe as a “netarchy”: “hierarchies within the network that own and control participatory platforms” while maintaining the illusion of distributed governance (Bauwens, Kostakis, and Pazaitis, Peer to Peer: The Commons Manifesto (University of Westminster Press, 2019)).

Compare all of this to the NAR/DAR framework. The rules are published. The Association’s authority is constrained by the locked protocol and by the requirement for court orders. Every action taken under DAR is visible to the entire network. There are no secret coalitions, no private governance agreements, no invisible coordination. The governance structure is less concentrated, more transparent, and more accountable than any on-chain voting mechanism — precisely because it operates through published rules and judicial process rather than through the aggregation of anonymous economic power.

IX. Distinguishing Protocol Immutability from Enforcement Action

A point that requires explicit treatment — and that the former employee’s argument trades on conflating — is the distinction between three categorically different kinds of action:

Alteration of consensus rules: changing the protocol specification itself — the block size, the scripting language, the supply schedule, the consensus mechanism. This is what BTC Core does when it implements SegWit or Taproot, and what the Ethereum Foundation did with the DAO fork and the Merge.

Alteration of transaction-validity conditions: changing which transactions are valid under the protocol rules. This would constitute a protocol change and would fall within category (1).

Enforcement action within an unchanged protocol: executing a freeze or reassignment of specific UTXOs pursuant to a court order, without altering the protocol rules themselves. The consensus rules remain identical. The scripting language is unchanged. The block structure is unchanged. What has changed is the spendability status of particular outputs, pursuant to a judicially authorised directive transmitted through a published system.

DAR operates exclusively in category (3). The former employee’s argument treats it as though it were category (1) or (2). That conflation is the analytical error at the heart of his position.

The distinction matters because the CLARITY Act’s “control” test is directed at category (1): the ability to unilaterally alter the rules or functionality of the system. A system in which the rules are fixed and published, and in which enforcement actions occur only through judicial process within those fixed rules, is structurally different from a system in which the rules themselves can be changed by an informal group of developers without published constraints.

A hostile reader might respond: “You are altering the legally operative state of assets and calling it non-governance because you define protocol change only at the code-specification level.” That objection has rhetorical force, but it proves too much. Every financial system in existence alters the legally operative state of assets pursuant to court orders — banks freeze accounts, registries update title records, exchanges halt trading in specific instruments — without thereby becoming “controlled” by the court system. The distinction between changing the rules and applying the rules to specific facts is foundational to every legal system. It is the difference between a legislature and a court. The existence of courts does not make a legal system “controlled” by courts. The existence of DAR does not make BSV “controlled” by the BSV Association.

That said, the fact that an organised notary-blacklist-alert pipeline exists — that there is a specific institutional mechanism through which court orders are translated into technically binding network outcomes — does create what might be called a privileged institutional chokepoint. This is worth acknowledging rather than dismissing. The response is not that the chokepoint does not exist. It does. The response is that it is constrained (by the requirement for court orders), transparent (published rules, public court proceedings), and accountable (judicial oversight, appellate review) — and that those constraints make it fundamentally different from the unconstrained, unpublished, unaccountable chokepoints that exist in BTC Core’s GitHub repository and in the Ethereum Foundation’s mandate.

The question is whether constraint and transparency are sufficient to neutralise the chokepoint for regulatory purposes. The argument that they are rests on four propositions.

First, the chokepoint cannot be activated unilaterally. No individual, no board member, no Association employee can trigger a freeze or reassignment without a court order. The trigger is external to the Association and lies within a separate branch of institutional authority — the judiciary. This is structurally different from a developer who can merge a pull request, or a foundation leader who can direct a hard fork, on their own authority.

Second, the chokepoint operates within a fixed and public rule set. The NAR specifies the conditions under which the alert system operates, the form of court orders that will be accepted, and the jurisdictions whose orders are recognised. These rules are published in advance and cannot be altered by the Association at its discretion. A bank can change its terms of service; the Association cannot change the NAR without publishing the change and subjecting it to the same unilateral-contract framework that governs participation.

Third, every exercise of the chokepoint is publicly observable. The alert is broadcast to the entire network. Every miner sees it. Every researcher can audit it. Every interested party can verify whether a court order exists and whether it meets the NAR’s requirements. This eliminates the information asymmetry that characterises opaque governance — the kind of asymmetry that securities regulation is specifically designed to address.

Fourth, every exercise of the chokepoint is judicially reviewable. The underlying court order can be challenged on appeal. The recognition of a foreign judgment can be contested. The cross-undertaking in damages provides a financial remedy if the order was wrongly granted. There are layers of institutional scrutiny that no on-chain governance mechanism replicates.

A system that satisfies all four conditions — external trigger, fixed public rules, observable exercise, and judicial reviewability — is not merely “constrained.” It is structurally incapable of the kind of discretionary, opaque, unaccountable control that the CLARITY Act’s maturity test is designed to detect. Whether a regulator will agree with that analysis is an open question. But the analytical foundation is sound.

X. The Real Question: What Does the CLARITY Act Require?

The CLARITY Act has passed the House of Representatives. It has not yet passed the Senate, where the competing Responsible Financial Innovation Act (RFIA) takes a different approach (Patomak Global Partners, ‘The Future of U.S. Crypto Regulation: Analyzing the CLARITY Act and the RFIA’, August 2025). The final statutory language may change. But on the terms of the current text, the comparative analysis is instructive.

BSV’s governance structure is relatively well aligned with the maturity criteria. The protocol is functional and processes transactions at enterprise scale. The code is open source. The rules — including the NAR — are pre-established, published, and transparent. The protocol is locked and cannot be altered by any party. Whether BSV would receive formal maturity certification is a regulatory question that cannot be prejudged.

BTC Core’s governance structure is less well aligned. The code is open source and the system is functional. But it does not operate upon “pre-established, transparent rules” in the sense contemplated by the Act — the rules change whenever the developer group decides to change them, through an informal process with no published governance framework. And whether BTC is “controlled” by the developer group depends on how seriously one takes the word “control.” If a handful of people with commit access to the reference implementation can change the protocol, reject proposed changes, and impose controversial modifications over community objections — and they can, and they have — then the maturity question arises.

Ethereum faces similar difficulty. The Foundation exercises significant influence over protocol development. Its co-founder selects its leadership and authors its mandate. Over 60% of staked ETH is reportedly controlled by a few entities. The protocol has been fundamentally altered multiple times without any published governance framework constraining the process.

The point is not that the CLARITY Act definitively classifies any of these networks. It does not — the Act establishes a certification process that has not yet been applied. The point is that the former employee’s claim that BSV uniquely fails the maturity test, while BTC and Ethereum pass it, inverts the comparative reality.

XI. Conclusion

The former employee’s core claim — that DAR and NAR constitute discretionary centralised control — does not survive examination of the primary documents. DAR requires a court order. The process involves adversarial litigation, judicial scrutiny, cross-border recognition proceedings, and costs that are prohibitive for all but significant claims. The NAR is a published, bilateral contractual framework that constrains the Association as much as it constrains participants. The protocol is locked.

The broader claims — that BSV fails the CLARITY Act’s maturity test, that BSV satisfies the Howey framework — are presented as settled conclusions. They are not. They depend on contested interpretations of statutory language that has not yet been applied by any regulator to any blockchain, and on fact-sensitive analysis that cannot be conducted in a social media thread.

What can be said with confidence is this: a blockchain that publishes its governance rules, locks its protocol, requires court orders for asset recovery, and operates through a transparent contractual framework is structurally more constrained and more accountable than one governed by an informal developer oligarchy with no published rules, no contractual framework, and no accountability mechanism. Whether that structural advantage translates into a formal maturity certification under the CLARITY Act is a question for regulators, and one that depends on fact-sensitive analysis that has not yet been conducted. The comparative analysis presented here does not prejudge that outcome, but it does identify the structural features that a consistent application of the statutory criteria would need to address.

The concern about concentrated ecosystem funding is legitimate and should be addressed on its own terms — through structural reforms to Association governance, through diversification of funding sources, and through transparent disclosure. That is a governance-maturity question, not a securities-classification question. Conflating the two does not protect BSV. It obscures the real issues and hands ammunition to regulators who may not understand the distinction between a locked protocol with court-order compliance and a mutable protocol with developer discretion.

The technology matters. The legal architecture around it matters more. And getting the legal architecture right — transparent, constrained, judicially mediated — is precisely what the CLARITY Act’s maturity test is designed to reward.

References

Cases

Adams v Cape Industries plc [1990] Ch 433 (CA)

Allcard v Skinner (1887) 36 Ch D 145 (CA)

American Cyanamid Co v Ethicon Ltd [1975] AC 396 (HL)

Carlill v Carbolic Smoke Ball Co [1893] 1 QB 256 (CA)

Cheltenham & Gloucester Building Society v Ricketts [1993] 1 WLR 1545

Clarke v Earl of Dunraven (The Satanita) [1897] AC 59 (HL)

Conservative and Unionist Central Office v Burrell [1982] 1 WLR 522 (CA)

Hedley Byrne & Co Ltd v Heller & Partners Ltd [1964] AC 465 (HL)

Mareva Compania Naviera SA v International Bulkcarriers SA [1975] 2 Lloyd’s Rep 509 (CA)

Re Grant’s Will Trusts [1980] 1 WLR 360

SEC v Coinbase Inc and Coinbase Global Inc (SDNY, 6 June 2023)

SEC v Ripple Labs Inc (SDNY, 2023)

SEC v W.J. Howey Co. 328 U.S. 293 (1946)

SEC v Glenn W. Turner Enterprises Inc. 474 F.2d 476 (9th Cir., 1973)

Williams v Carwardine (1833) 5 C & P 566

Winter v Natural Resources Defense Council 555 U.S. 7 (2008)

Legislation

Civil Procedure Rules 1998 (SI 1998/3132), Part 25, r. 5.4C

Consumer Protection from Unfair Trading Regulations 2008 (SI 2008/1277)

Digital Asset Market Clarity Act of 2025 (CLARITY Act), H.R. 3633, 119th Congress (2025–2026)

Federal Rules of Civil Procedure, Rule 65

Hague Convention on Choice of Court Agreements 2005

Partnership Act 1890

Securities Exchange Act of 1934, §13(d)

Senior Courts Act 1981, s. 16

Secondary Sources

Bauwens, M., Kostakis, V. and Pazaitis, A., Peer to Peer: The Commons Manifesto (University of Westminster Press, 2019)

BSV Association, ‘Network Access Rules’, Version 1 (15 February 2024), available at nar.bsvblockchain.org

BSV Association, ‘Protecting Assets, Ensuring Justice: BSVA’s Alert System and DAR Framework’ (2024)

BSV Association, ‘Digital Asset Recovery and the Law’ (2024)

BSV Association, ‘The Importance of Digital Asset Recovery’ (2024)

BSV Association, ‘Taking the Complexity out of Digital Asset Recovery’ (January 2025)

BSV Association, ‘Unravelling Blockchain Governance: The BSVA’s Approach to Network Stewardship’ (14 March 2024)

BSV Association, ‘ELI5: BSV Network Access Rules’ (June 2024)

Nakamoto, S., ‘Bitcoin: A Peer-to-Peer Electronic Cash System’ (2008)

Wright, C.S., Fiduciary Governance of BTC Core under English Law (PhD thesis, University of Leicester, 2025; forthcoming as peer-reviewed monograph, Ethics Press, 2026)

Zou, M., ‘Cryptocurrency and Blockchain Governance’ in Regulation of Crypto-Assets (Hart Publishing, 2024)

Walch, A., ‘In Code(rs) We Trust: Software Developers as Fiduciaries in Public Blockchains’ in Hacker, Lianos, Dimitropoulos and Eich (eds), Regulating Blockchain: Techno-Social and Legal Challenges (OUP, 2019)

Walch, A., ‘Deconstructing “Decentralization”: Exploring the Core Claim of Crypto Systems’ in Brummer (ed), Cryptoassets: Legal, Regulatory, and Monetary Perspectives (OUP, 2019)

Hofman, D., DuPont, Q., Walch, A. and Beschastnikh, I., ‘Blockchain Governance: De Facto or Designed?’ in Lemieux and Feng (eds), Building Decentralized Trust: Multidisciplinary Perspectives on the Design of Blockchains and Distributed Ledgers (Springer, 2021)

Bitcoin Core Project, ‘About’ (bitcoincore.org)

Bitcoin Core Project, CONTRIBUTING.md (github.com/bitcoin/bitcoin)

bitcoin++, ‘Bitcoin Core Adds New Maintainer: sedited’ (10 January 2026)

Arnold & Porter, ‘Clarifying the CLARITY Act: What To Know About the House Crypto Market Structure Bill and Its Path to Law’ (August 2025)

Congressional Research Service, ‘Crypto Legislation: An Overview of H.R. 3633, the CLARITY Act’, IN12583 (2025)

DLA Piper, ‘Digital Asset Market Clarity Act: The Increasing Role of the CFTC in Regulating Crypto Markets’ (June 2025)

Patomak Global Partners, ‘The Future of U.S. Crypto Regulation: Analyzing the CLARITY Act and the RFIA’ (August 2025)

De Silva Law Offices, ‘Crypto Market Bill Explained: The CLARITY Act of 2025 & Digital Asset Regulation’ (May 2025)

The Barrister Group, ‘Can Bitcoin Help Recover Bitcoin? Balancing Decentralisation and Complying with Court Orders’ (January 2025)

Thank you, Dr. Wright, you are amazing!

If I were to attempt a DAR on BTC assets, using NAR/DAR 'manually', that is without it needing to be explicitly implemented as it is with BSV, I'm sure it would be a harder task. But would it still work and re-assign assets to the legal owner?

In short, why bother with NAR/DAR if so and what is the motivation of it?

BTW concerning the 'former employee' you have not told us clearly how his main concern is that even though your are correct in every way technically and legally, the US Treasury will ignore all those trifles as they have done with BTC and the Strategic Bitcoin Reserve. You even point this out with great clarity in this very article. Thus once again putting BSV in a very poor position with the people of the world because it will not be adopted if the state continues in this way.

You wrote an excellent piece last week confessing to have made this kind of worldly mistake before and regretted it which is the sign of an honourable man. Now you seem to be lacking the wisdom to deal with politics here again.

This is not an attack on you. It is saying why not listen to his key point about giving BSV the highest chance of success when dealing with the state which always changes its own rules - this is life, the way of the world.

The grace of God has already forgiven the world for its sins. This is a job you do not have the power to do nor should you be trying.